National AI office demand is up 85% year-over-year, and 179% in the major AI hubs. CB Insights reports US private AI funding hit $206 billion in Q1 2026 alone, close to the full-year 2025 total of $217 billion. The headline rate obscures the more consequential finding.

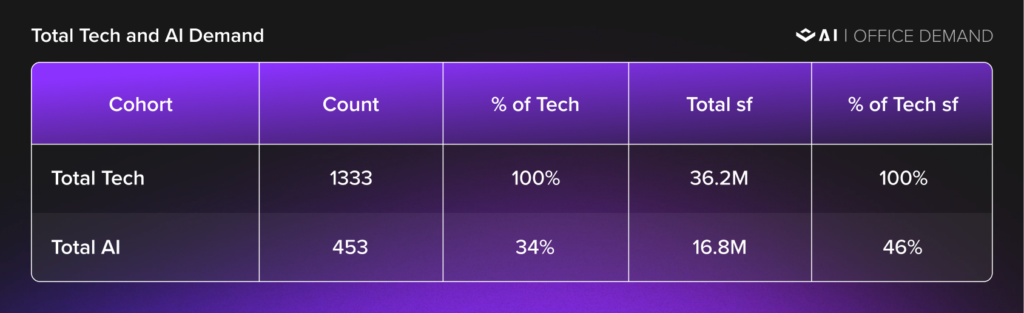

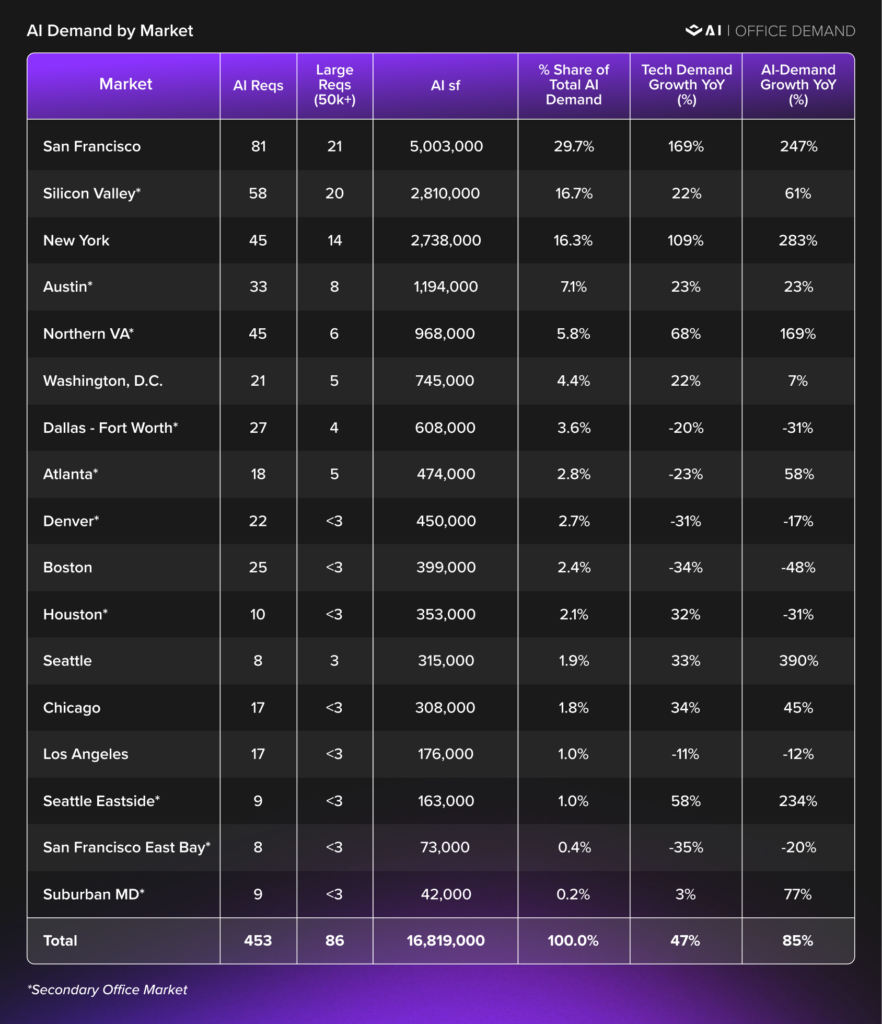

This growth is not lifting the sector evenly. It is pouring into a small set of submarkets at a pace that is driving availability in those corridors lower even as surrounding submarkets stay loose. Of the active tech requirements VTS is tracking across the seventeen markets, 34% are AI, and those 453 requirements account for 16.8 million square feet. Three metros claim 63% of that square footage, and a single submarket contains 25%.

The Capital Backdrop

Q1 2026 was the largest funding quarter in the AI sector’s history. Global private AI funding reached $226 billion, a 216% jump from Q4 2025's $72 billion. The U.S. captured $206 billion across 980 deals, and 94% flowed through mega-rounds of $100 million or more. Silicon Valley alone took in $190.7 billion, more than the US AI sector raised in any year before 2024.

Three Bay Area names lead the list. OpenAI alone closed $122 billion at an $840 billion valuation. Anthropic and xAI added another $37.5 billion between them. The engineering talent that converts this capital into office demand is concentrated in a handful of cities.

What This Capital Creates

In the post-GFC recovery, San Francisco Tech employment grew 90% from its May 2010 trough through December 2019; Professional Services and Finance grew 26% over the same period, and did not begin recovering until April 2011, one year after Tech employment bottomed. In New York there was virtually no lag as Professional Services and Tech employment both hit their GFC troughs in August and December of 2009 respectively with Finance shortly thereafter in January 2010. All three employment segments gradually started their GFC recovery in early 2010. In the post-GFC recovery, Tech employment was outperforming Finance but it did not establish itself as a leading industry demand driver in New York until 2015. Nationally, the lag from Tech inflection to Professional Services recovery ran about 12 months. That is roughly how long it takes services firms to see enough sustained client activity before committing to new space.

In the twelve months through May 2026, tech requirement velocity across all markets VTS tracks is up 47%. Professional services velocity is moderately up by 3%, Finance is down 13%, and legal is down 16%. That lag hasn't appeared nationally yet. Conversely in San Francisco, Tech requirement velocity is up 169% TTM while Professional Services and Finance are up 33% and 13% respectively, while Legal in San Francisco is down 51%.

Prior cycles suggest Professional Services requirement velocity follows Tech with approximately one year lag. The Professional Services growth of 33% TTM in San Francisco, the market with the highest AI concentration, is consistent with early pull-through. Legal demand nationally is down 16% and in San Francisco down 51%, which could reflect either AI automating legal work in real time or a correction from an unusually high 2024. Both are probably contributing, but a correction from a strong 2024 is the cleaner explanation.

If VC investment slows, the demand will look different from 2022. Then, tech companies had over-hired ahead of revenue, and when funding contracted, companies cut headcount quickly. The largest AI tenants today are scaling revenue faster and from a higher base, and organizations that have committed to AI deployments are years from completing deployments they have already committed to. A funding correction would slow demand growth, but would be unlikely to produce the retrenchment that 2022 did.

AI is also generating demand across use cases that share little except the infrastructure they run on. Washington D.C.’s AI concentration in the East End is driven by defense procurement. Anduril, Shield AI, and the consultancies on Pentagon AI contracts, while often VC backed, drive revenue through a different mechanism that responds more to the defense budget than to VC funding trends.

AI Is Now the Tech Demand Story

Among the Tech requirements VTS tracks, AI tenants now account for nearly half of all active square footage. AI requirements are 34% of the count but 46% of the active Tech square footage, as the table below shows.

The skew is in the size of the average deal. AI requirements average 37k square feet, compared to 27k square feet for the tech requirements overall, a difference of 37%.

91 AI requirements are at 50k square feet or more, accounting for 71% of all active AI square footage. The 50k+ enterprise tier is back after three years of downsized Tech renewals, with 74% of that square footage concentrated in just six submarkets: SF Non-Core CBD, San Jose, Midtown, Midtown South, SF South Financial District, and Austin Non-CBD.

Market-Level Concentration

San Francisco, Silicon Valley, and New York account for 41% of the active AI requirements and 63% of the active AI square footage. San Francisco alone sits at 5.0 million square feet, nearly a third of the national total. The VTS data below shows year-over-year growth in Tech and AI active demand by market, alongside AI’s share of total active Tech square footage in each.

In the post-GFC cycle, San Francisco anchored in 2010, New York followed by 2013, and Seattle entered the picture by 2016. The current cycle has compressed that sequence. SF, Silicon Valley, and New York are the primary hubs, and Seattle, Northern VA, and Austin are already showing early growth signals.

A Handful of Anchors Drive San Francisco Demand

San Francisco's 81 active AI requirements average 62k square feet, 2.3 times the average tech requirement across all markets VTS tracks. Per public reporting in the SF Standard and San Francisco Chronicle, Sierra Technologies (the agentic AI startup co-founded by OpenAI Chairman Bret Taylor) is set to lease ~300k square feet at 185 Berry Street and is scouting additional space across the SoMa / South Beach corridor, OpenAI continues to add to its Mission Bay base, and Anthropic added new San Francisco requirements in Q1 2026. Those same public sources put AI-related occupancy in San Francisco at 5.0 million square feet.

New York's Different Tenant Mix

New York's 45 active AI requirements average 61k square feet, and 14 are at 50k square feet or more. Unlike San Francisco, which is dominated by foundation-model labs, New York skews toward application-layer AI tenants and AI infrastructure companies serving enterprise customers, reflecting the city’s financial, legal, and media base. Much of the recent leasing is for growth space, with tenants taking more square footage than headcount requires.

The most visible Q1 2026 deal was Nscale Global Holdings, an AI cloud infrastructure company fresh off a $1.6 billion Series C at a $14.6 billion valuation, which signed for ~7,200 square feet at One Vanderbilt at $320 per square foot, the highest office rent ever recorded in Manhattan. Harvey AI (legal AI, $11 billion valuation), ElevenLabs (voice/audio AI, $11 billion valuation), and Agentio (AI advertising) are all active in Manhattan.

Adoption is moving fastest in coding and creative workflows and more slowly in enterprise functions with complex systems and sensitive data, which partly explains why New York’s application-layer AI tenants are scaling differently from San Francisco’s foundation-model labs. In order to help accelerate the adoption of these new technologies, recently investment firms such as Brookfield and Blackstone have ventured with OpenAI to start deploying engineering talent to its portfolio companies across the nation. These types of moves will help in speeding up the expansion and broaden the demand for AI labor outside of the two core markets it's currently entrenched in.

Seattle, Chicago, and Washington, D.C.

Seattle: Seattle has the highest AI growth rate of any market VTS tracks: 390% year-over-year, reaching 315k square feet. AI’s share of active tech demand is 61%. The largest requirements are from out-of-town tenants, with a mix of pure-play AI firms and larger enterprises making AI-adjacent moves. Seattle’s deep AI engineering talent pool is the pull.

Chicago: Chicago shows the Seattle pattern at lower intensity: AI demand up 45% year-over-year, growing to 308k square feet, and AI is only 22% of total tech demand. Most of it sits in the West Loop / Fulton Market corridor, where Google’s Midwest HQ anchors a tech worker base. The Chicago AI thesis is enterprise deployment into manufacturing, logistics, healthcare, and financial services rather than foundation-model research.

Washington, D.C.: AI active demand in D.C. is up 7% year-over-year, with total volume at 745k square feet. AI's share of local tech demand is unusually high: 80.7% in DC Non-Core, 75.8% in East End, 69.5% in D.C. CBD, 67.6% in Capitol Hill. Anduril ($30.5B valuation), Shield AI ($12.7B), Palantir, and the consultancies working on Pentagon AI programs account for most of that demand, driven by the region's defense procurement and policy work.

Los Angeles and Boston

Neither market is part of the AI demand picture. LA AI demand is down 12% year-over-year, Boston is down 48%, AI accounts for 16% of tech demand in LA; Boston's 46% share reflects a smaller tech base rather than AI strength. Total AI square footage is 176k in LA and 399k in Boston, together just 3% of the national total. LA's South Bay cluster shows a 76.6% AI concentration driven by aerospace and robotics firms, and Boston's Seaport shows an 88.5% AI concentration driven by a small number of specialized firms, but both reflect submarket specialization rather than broad market demand.

Silicon Valley, Austin, Northern Virginia, and Atlanta

Silicon Valley's 58 active AI requirements total 2.8 million square feet, 60% of all active tech demand in the market. Nearly all of it sits in San Jose. The tenant profile here is distinct from San Francisco's foundation-model labs: the dominant firms are in chip design, AI hardware, and inference infrastructure, drawn by proximity to semiconductor supply chains rather than engineering talent pools. San Jose is its own cluster, not an extension of SF.

Austin has 33 active requirements totaling 1.2 million square feet, up 23% year-over-year, with 48% of active tech demand coming from AI tenants. The large requirements are driven by established tech incumbents expanding existing Austin footprints at lower cost than the Bay Area, rather than AI-native firms opening new markets.

Northern Virginia is up 169% year-over-year to 968k square feet, the strongest growth rate of any secondary market VTS tracks. AI accounts for 57% of active tech demand. The concentration runs along the Rosslyn-Ballston corridor, where the demand profile is federal: defense contractors, intelligence-community-adjacent firms, and government technology integrators. AI demand in this cluster is driven by procurement, not commercial adoption.

Atlanta is 474k square feet across 18 requirements, up 58% year-over-year. AI accounts for 28% of active tech demand. The tenant base skews toward enterprise software firms with AI components rather than pure-play AI, and the demand is spread across Atlanta CBD and the suburbs rather than concentrated in a single node.

Submarket Concentration: One Cluster, 25% of Active AI Demand

The market-level data understates the concentration. At the submarket level, a single cluster (SF Non-Core CBD, covering the SoMa / Howard Street / Mission Bay corridor) leads by a wide margin with 46 active AI requirements. The next four clusters by absolute AI demand are SF South Financial District (2.69M square feet), San Jose (2.42M square feet), Midtown South (1.90M square feet), and Midtown (1.39M square feet).Those five clusters account for the bulk of enterprise-scale AI demand nationally.

The highest absolute demand clusters sit in San Francisco, Silicon Valley, and New York. Among clusters with material square footage, the highest AI concentration rates sit in East End (75.8%), SF Non-Core CBD (72.8%), San Jose (67.4%), DC CBD (69.5%), and Midtown (61.2%). In those submarkets, AI accounts for effectively all active tech demand.

SoMa, Howard Street, and Mission Bay

The AI demand in the most concentrated cluster is already touring, signed or in active negotiation. Led by foundational leaders in the space: OpenAI's search, Anthropic's expansion, Sierra's pending ~300k-square-foot requirement at 185 Berry, and dozens of mid-sized requirements have all clustered in the same handful of buildings.

Midtown South and Midtown

Nearly all of New York's active AI demand (2.7 million square feet across 41 of the market's 45 AI requirements) is in Midtown or Midtown South. Midtown South concentrates the venture-backed, application-layer AI tenants, with requirements ranging from 5k to 30k square feet and several larger anchor users. Midtown, anchored by trophy buildings like One Vanderbilt and Hudson Yards, has captured the enterprise AI infrastructure tenants willing to pay premium rents. The Nscale deal at $320 per square foot crystallizes the Midtown pattern: AI infrastructure tenants paying record rents for trophy space.

Seattle’s Incoming Enterprise Tenants

All 8 active AI tenants, totaling 315k square feet, are looking in the Core CBD and Lake Union/Denny Regrade. A number of locally-founded tenants (AI research institutions, infrastructure firms, and smaller startups) sit alongside them, but incoming tenants are driving most of the demand.

Concentration vs. Diffusion: Will the AI Boom Follow Previous Tech Cycles

VTS Data reflects demand from well funded early movers: the foundation-model labs and application firms such as OpenAI, Anthropic, and Sierra, which draw AI engineering talent on name alone. The next phase will be driven by service-providing sectors: healthcare, financial services, and manufacturing. The expansion will also reach other large labor markets: Chicago, Los Angeles, Atlanta, and Austin. Three pressures will push demand outward: AI engineering talent is scarce, San Francisco real estate is expensive, and 25% of active AI demand concentrated in a single submarket will produce the crowding that pushed prior cycles outward. Seattle's 390% year-over-year AI demand growth is an early signal of that dynamic.

But in this AI-driven tech expansion, disruption and concentration are happening simultaneously. According to ADP Research, jobs in roles such as software development and customer service have declined 6% for workers aged 22 to 25 between late 2022 and July 2025. During that same period, employment among workers 30 and older for those same job categories grew by 6 to 13%. Growth in these fields is concentrated at the senior end and in firms that need specialist talent to solve problems rather than pure task-based work driven by absolute headcount. The foundational labs driving this renaissance are not software companies, they are more akin to research organizations with specialized talent that does not transfer easily to other markets. Neither of these dynamics guarantees that demand will diffuse broadly the way prior tech cycles did.

Bottom Line

The VTS data shows AI office demand concentrating at the submarket level in ways that metro-level vacancy statistics obscure. Landlords and investors underwriting to market averages are mispricing both sides: despite high vacancy rates, concentrated AI demand is driving availability meaningfully lower in a handful of corridors, while the rest of the markets VTS tracks are seeing little AI benefit.

The submarket concentration today mirrors how tech demand was distributed at the start of the last two cycles, before professional services and secondary markets followed.

Want to see the real-time demand shifting in your specific markets? Click here to book a demo and learn more about VTS Data.

Stay on top of our latest updates